[ad_1]

Fisker Stock Analysis David Ramos

Thesis

Fisker (NYSE:FSR) is a much talked about stock, with bears and bulls arguing over which thesis is right. And at the moment, the sentiment is a little more negative on this stock as the cuts in the guidelines and the economic environment take their toll. However, times like these could be the perfect opportunity for long-term investors. I think this month will be an important point when the first few thousand cars are delivered and the first reviews are written. They could send the shares soaring or they could lead to further falls.

Analysis

A German car influencer, who regularly updates his followers on the delivery process, received a delivery date between 14 and 30 June and will be one of the first owners worldwide, being in the first batch. As his video is in German, which you can watch here, I will bring you up to date on some of the points he made about the car and the pick-up process.

Fisker customers can use Allego (ALLG) charging points for free for 1 year and a partnership with Allianz Partner offers 100k km roadside assistance. They are also building / negotiating with partners to set up a bodyshop network. And Bridgestone (OTCPK:BRDCY), with its Pitstop brand, could be the partner for maintenance and repairs. According to the influencer, the battery warranty is likely to be 160k km or 10 years.

Some critics said Fisker would never deliver cars, so this month will be interesting and especially the results later this year when they have had a few months of delivered cars should answer a lot of questions. Delivery will be key, as reservations can be cancelled quickly and competitors’ cars are available more quickly. So what matters is how quickly Fisker can produce and deliver its cars. And it is the actual delivery time that counts, not the guidance given now, which may have to be adjusted.

Fisker Ocean Against The Competition

Henrik Fisker was involved in the design of the stunning Aston Martin (OTCPK:AMGDF) DB9 and V8 Vantage, so he clearly has a feel for beautiful car design. And his Fisker Ocean looks quite similar to the Range Rover Evoque, which has been a huge success and is very popular in Europe. A common argument is that Fisker is the first affordable SUV for the mainstream, and I have to say that this is not entirely true, as cars like the VW (OTCPK:VWAGY) ID4 or the Hyundai (OTCPK:HYMTF) Ioniq 5 are in the same price category as the base model. And at the top end of the Ocean price spectrum, they also compete with Tesla (TSLA), Mercedes (OTCPK:MBGAF) and more.

And the counter argument from people who are negative about Fisker is that these cars are available now and Fisker needs to start delivering their cars. But due to the earlier approval in Europe and the fact that the EPA has confirmed the 360 mile range + approval for sales and delivery in the US, this argument could be obsolete. Deliveries to the US will start on 19 June and it is now important that Magna Steyr (MGA) can ramp up production.

Magna, which has a nearly 10% stake in Fisker, has a vested interest in the economic success of the company as it is a shareholder. However, it should be noted that this is due to the right to exercise warrants held by the company. But Magna, which has a lot of experience in the automotive sector through its production of EVs for Jaguar, must now prove whether the asset-light model was the right one for Fisker and whether it can scale up production quickly enough.

For the production of the next model, the PEAR, Fisker is working with Foxconn (OTCPK:FXCOF), which has much less experience in the automotive industry, and it will be interesting to see how this works out in the future.

The target for the end of the year is 6,000 cars per month, i.e. 72,000 over a 12-month period, so the order book is potentially secured for 1+ years, depending on how the first models delivered are received. But good or bad reviews could have a real impact on orders.

Future Growth Opportunities

China will be a big market in the future and with plans to open the first delivery center in 2023 and start deliveries in Q1 2024, Fisker is really trying to expand fast. China accounted for ~1/4 of global car sales in 2022. In the longer term, there should also be a plan to assemble cars in the US to take advantage of the federal EV tax credit program.

And perhaps the biggest challenge and most important aspect will be how they build their brand to sell more cars in the future and how they differentiate themselves from the competition. Tesla has managed to sell a huge number of cars without spending much on marketing and advertising, but they have Elon Musk, who uses social media heavily and is really talented at generating buzz. The old car manufacturers, on the other hand, spend a lot of money on marketing campaigns, so I would say that Fisker will have to invest in marketing in the future too, because I don’t see Henrik Fisker becoming the same celebrity as Elon Musk in the near future.

The automotive landscape is also very competitive. And at the moment Fisker does not have the competitive advantage that Tesla has with its brand and Musk’s personality. The asset-light model could be a competitive advantage in the future, but at the moment we cannot say for sure. We will have to see how their margins and car quality develop. There is a big difference between selling 20,000 cars a year and 200,000 cars a year and, as always in business, there will be unexpected problems. Depending on how the Foxconn situation develops, it could also be interesting to see how this plays out as Foxconn builds up a deep knowledge of manufacturing Fisker’s cars and if they try to leverage that power in the future.

In addition, if competitors see that the asset-light model works, they will adopt it and start attacking the moat, and that is always a critical point where companies succeed or get crushed. Fisker is a high-risk, early-stage investment where some competitors have an advantage due to better financials, years of supply chain development and more. But a small position could turn into something really big if they succeed, as the potential reward is huge. But nobody has a crystal ball to see the future, and right now there are a thousand variables that could affect the stock in either direction.

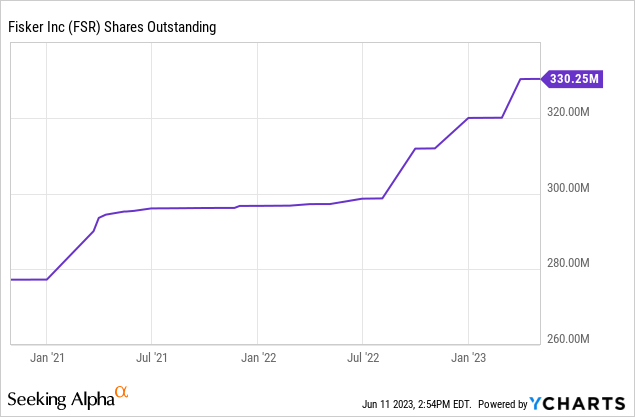

Shareholder dilution is always a concern with companies like Fisker, and depending on the development of the cash position and free cash flow, new money may be needed. Unfortunately, Fisker does not have Amazon (AMZN) as a partner like Rivian (RIVN), but I think Magna could be a potential financier and depending on the reviews of the first released models, there will be new prospects. As I said, the Ocean has to meet expectations and bad reviews could be very bad for existing shareholders.

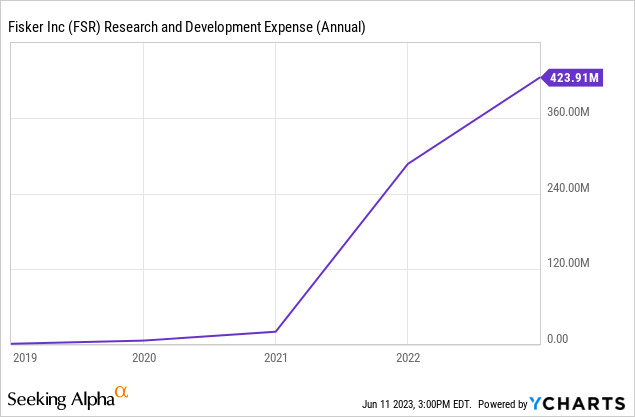

It is always important to me to keep capital allocation at a high level and I think investing in R&D now is the right thing to do in order to achieve high ROIC in the future when the company is a bit more mature. A strong UI/software will be a major differentiator in the future and I hope they can improve on that.

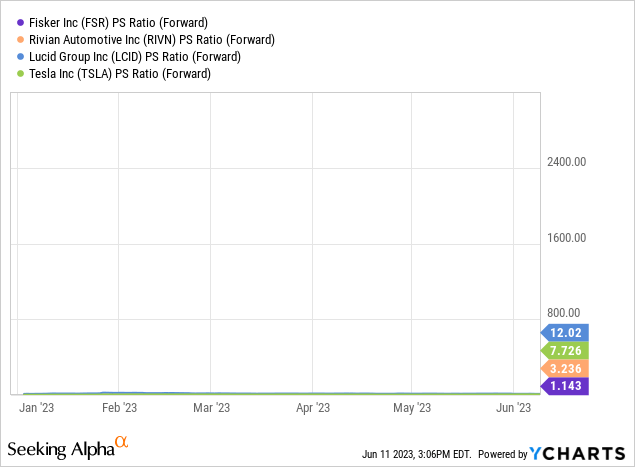

On a forward PS ratio, Fisker looks undervalued compared to some of its peers, but at such an early stage for 3 of the 4 companies, forward looking statements are very error-prone as even small changes can lead to very different results. But the others are trading at higher multiples because the market sees them as less risky due to their mix of financials and growth opportunities.

Henry Fisker is also often criticized for his previous failures with Fisker Automotive, but I would say that this could be a positive thing if he has learnt from them and now knows what he needs to do differently. There are many entrepreneurs who have failed many times before they succeed.

Conclusion

Before the first reviews come out, I would wait and see, because if Fisker really succeeds, there will be plenty of buying opportunities in the future. And a lot of people are trying to influence you by saying that if you don’t buy now, it will be too late because the shares will be too expensive. In my opinion, this is nonsense because you could have bought shares in Walmart (WMT) and Tesla many years after the IPO and still made x times your investment. Better to leave a few points of return on the table than to make an overly risky investment.

[ad_2]

Source link