[ad_1]

Michael Gonzalez

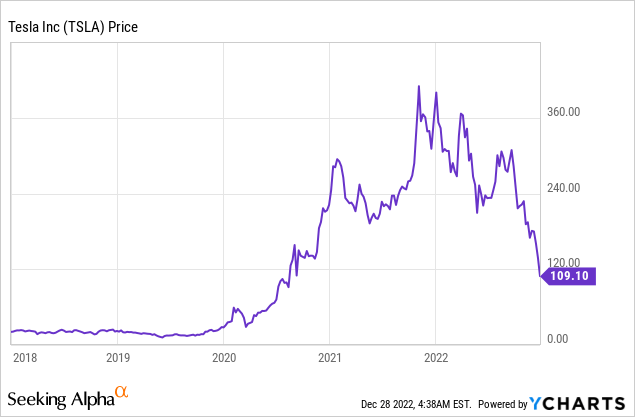

Tesla (NASDAQ:TSLA) is one of the world’s largest EV makers and one of the most popular stocks in the world. The company was catapulted into stardom during the stimulus-fueled bull market of 2020, which sent the company from near bankruptcy to an S&P 500, trillion-dollar titan. This tremendous bull run meant Tesla’s stock price increased by over 1,300% and made many investors “Teslanaires”. However, since the macroeconomic environment changed in November 2021, as the high inflation numbers were released, Tesla has become a rollercoaster for investors. The stock price has now been butchered by 73% from its all-time highs, with a 44% decline in December alone. This looks to have been driven by a series of macroeconomic factors. In addition, to a serious amount of stock selling by founder Elon Musk (which I will discuss more on in the Risks) section. There have also been some reports of a production cut in January 2023, expected at Tesla’s Shanghai factory. Although the company hasn’t confirmed this yet. With all this bad news you may wonder why I am bullish on the stock? There are a few reasons for this, of course, we know about the company’s leadership position and technology innovation. In addition, Tesla customers are now poised to benefit from a $7,500 EV tax incentive which was offered thanks to the “anti-inflation act” and should boost EV demand. Its stock is also deeply undervalued intrinsically. In this post, I’m going to review its financials, outline production updates, and revisit its valuation. Let’s dive in.

Strong Financials

Tesla generated strong financial results for the third quarter of 2022. Revenue increased by a rapid 56% year over year to a record $21.45 billion, which was a strong positive. However, it did miss analyst estimates by $428.34 million. This was mainly driven by unfavorable foreign exchange headwinds, as a rising dollar impacted international revenue. Overall vehicle deliveries increased by 42% year over year to 343,830 units. The Model Y drove the majority of sales, followed by the Model S.

The aforementioned tax credit is for EV vehicles that sell for below $55,000 and thus this includes Tesla’s best-selling models 3 and Y. However, with options attached to the models, this will likely go over the tax rate availability. I did notice Tesla has relatively few low-cost (below $50,000 models) available on its website, within 200 miles of Rodeo Drive LA. I suspect the tax credit has helped to boost sales of low-value models already, which is a positive. I did notice Tesla is offering 10,000 miles of free supercharging which looks to be an incentive to boost demand further.

Tesla vehicle stock (Tesla website, author search)

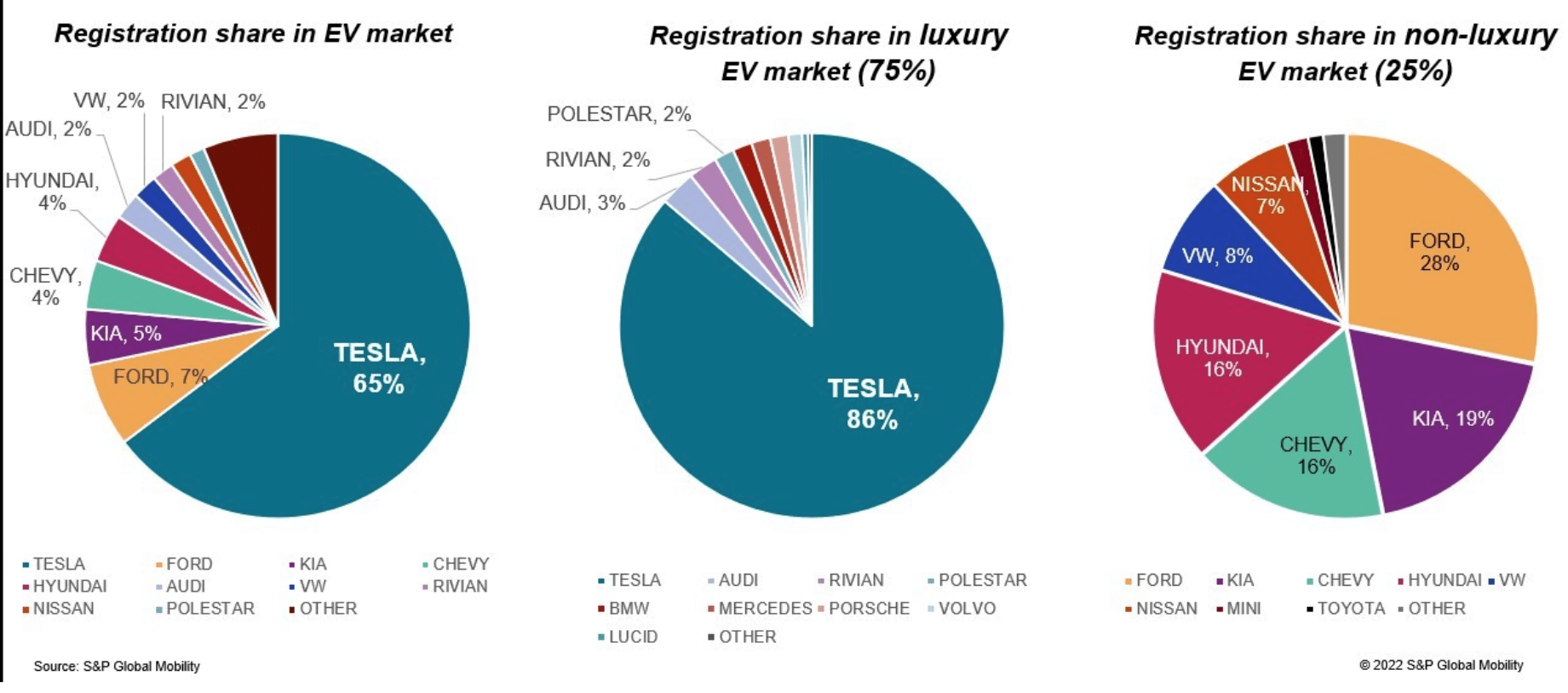

As of the third quarter of 2022, Tesla ramped up its production by 54% YoY to 365,923 vehicles. The latest data (November 2022) shows Tesla still dominates the electric vehicle market in the U.S.A, with 65% market share. However, it should be noted that its market share has declined from the 79% in 2020. For many years, bearish analysts have said “competition is coming” for Tesla, but now it looks as though they are finally starting to eat market share.

Tesla market share (Electrek)

Ford is the second largest EV maker in the U.S. but still trails Tesla massively with just 7% market share. The company produces the F-150 which is the most popular vehicle sold in the U.S. Its new EV version of the F-150 is forecast to be released in 2023 and thus I believe this will be a major driver of sales. A positive for Tesla is the entire EV market is growing and thus the pie is getting bigger for all manufacturers. According to one study, the EV industry is forecast to grow at a 23.1% CAGR and be worth over $1.1 trillion by 2030.

Ford 150 Electric (Ford Website, author screenshot)

A positive for Tesla is it doesn’t have to convert traditional internal combustion engine facilities into EV manufacturing plants, like many traditional automakers. Tesla is vertically integrated from the ground up and has even developed unique pieces of equipment to manufacture its cars, such as the world’s largest “gigapress”. Elon Musk has often stated in the past that producing a prototype or a low volume of vehicles is “pretty easy”, but manufacturing at scale is the challenging part. Tesla ramped up its Shanghai factory production in the third quarter and its Berlin factory also produced 2,000 model Y vehicles, although still in the early stages of a full ramp.

Tesla’s rate of innovation is so great that when traditional auto manufacturers are thinking about breakfast, Tesla is already eating their lunch. For example, I recently watched the Tesla Semi presentation by Elon Musk, which is currently in production. The company has reinvented trucking with a smooth design which was tested in a state-of-the-art wind chamber, to maximize its range of 500 miles which was astonishing. The truck is also reportedly as “easy to drive as a Model 3, with basically no training required” according to Musk.

Tesla Semi (Tesla)

Tesla has also innovated on the charging front with new “Megachargers” announced, that enable charging at a staggering 1 megawatt. This basically means truck batteries can be charged up to 70% in 30 minutes, which is the average amount of time a truck driver will take on a refresh break. The uniquely designed Cybertruck is also reported to start production in 2023 and will benefit from the “Megachargers”.

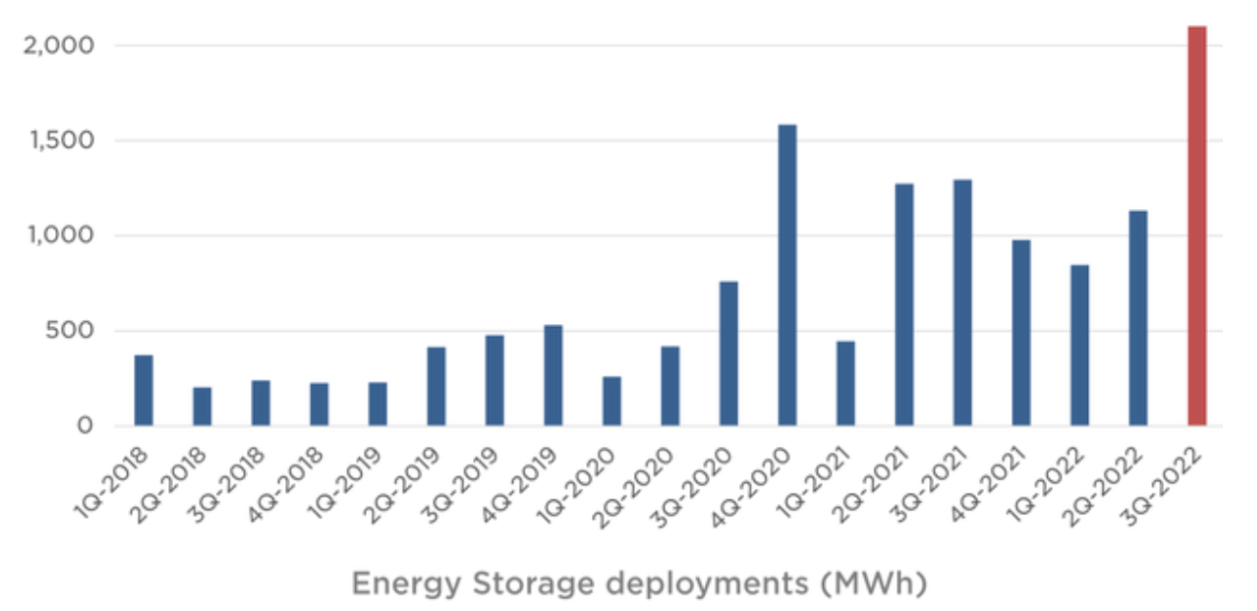

Tesla increased its energy storage deployed to 2,100 MWh, which increased by a substantial 62% year over year. The company did experience some supply chain constraints as demand continued to “outstrip supply”.

Energy storage (Q3,22 report)

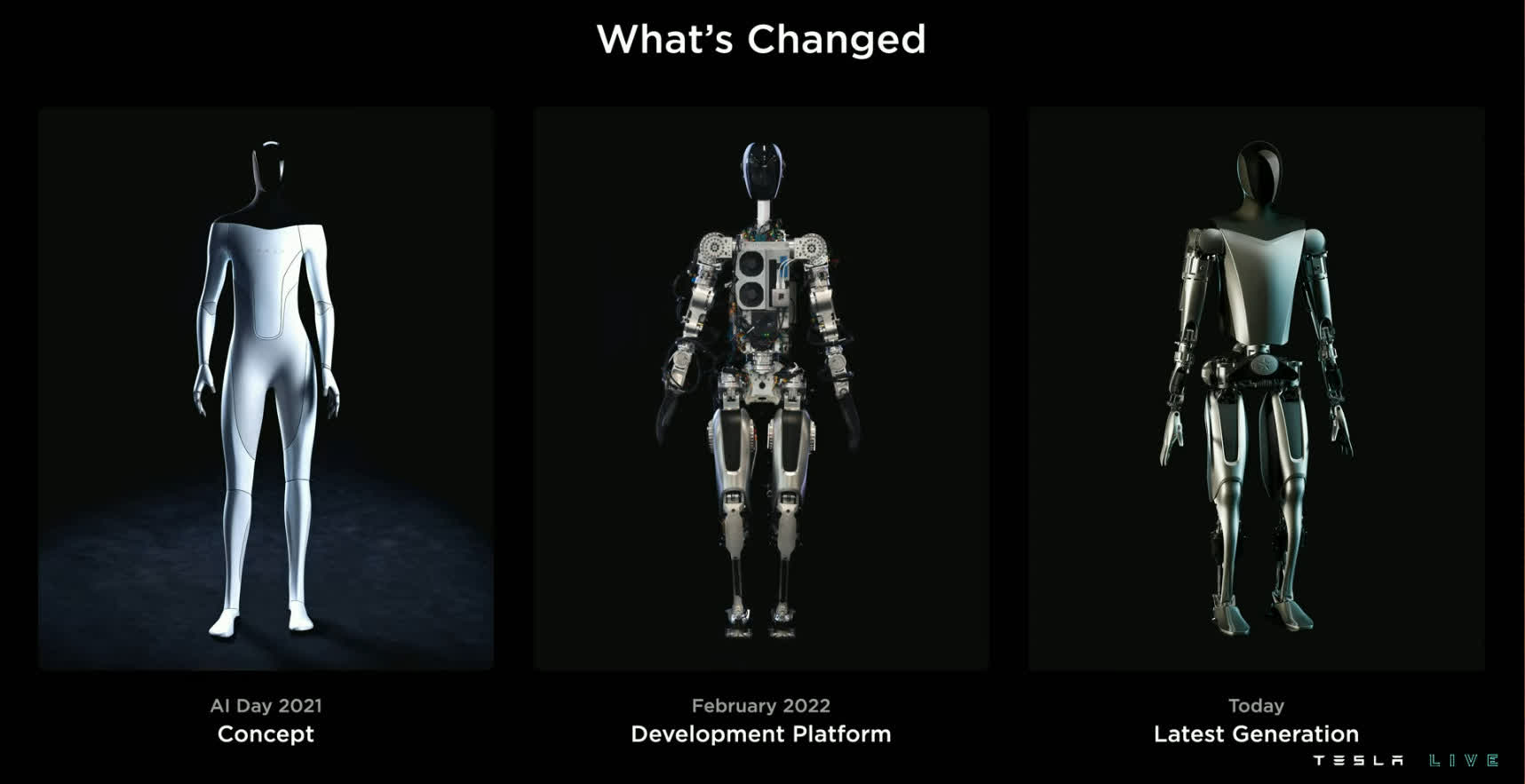

Tesla is also innovating on the artificial intelligence front as the company announced its beta Full self-driving and even humanoid robot concept called Optimus, which I have covered in greater detail in past posts. AI has recently seen a huge surge in popularity. The Open AI institute which was originally backed by Elon Musk released the popular ChatGPT, which some analysts believe could rival Google. I could envision a ChatGPT-like AI model embedded into the software of Optimus, which would make it a font of information while also assisting with tasks based upon prompts. This would truly create a “superintelligence” quite easily given the component pieces are all available.

Tesla AI Day 2022 (Tesla)

Tesla reported earnings per share of $0.95, which increased by a staggering 93.57% year over year and beat analyst estimates by $0.06. The company also has a strong balance sheet with $21,107 billion in cash and short-term investments. The company does have fairly high debt of $5.87 billion, but just $979 million of this is short term debt, due within the next 2 years.

Advanced Valuation

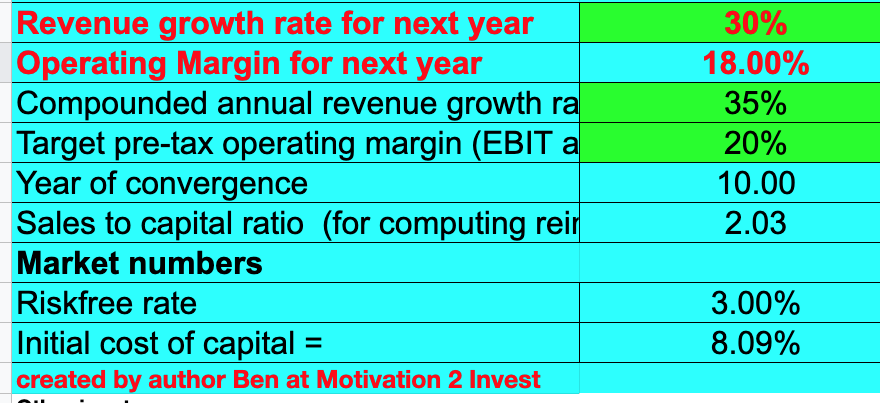

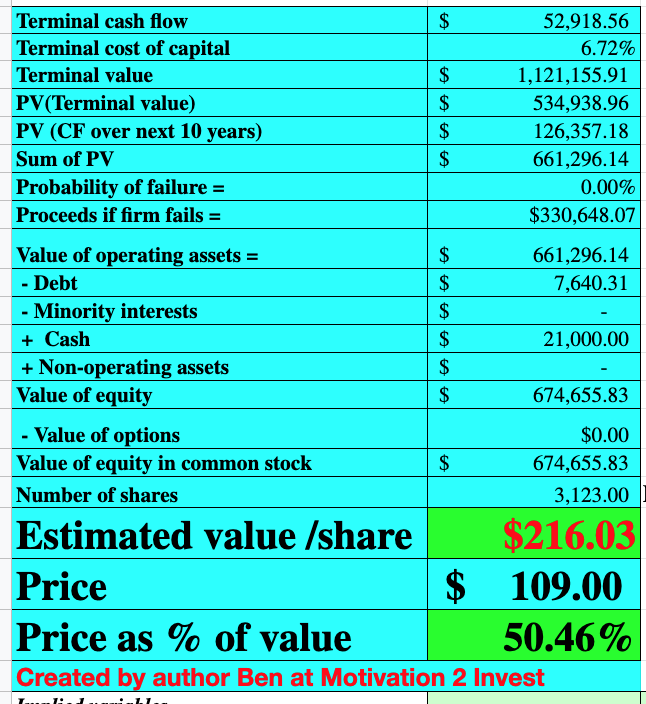

I have plugged the latest financials of Tesla into my discounted cash flow valuation model. I have forecasted 30% revenue growth for next year which is fairly conservative given past growth rates of above 50%. I have given a lower estimate due to the tepid macroeconomic environment forecasted. However, in years 2 to 5, I have forecasted a recovery with a 35% revenue growth rate per year.

Tesla stock valuation (created by author Ben at Motivation 2 Invest)

To increase the accuracy of the valuation, I have capitalized R&D expenses which has lifted net income. In addition, I have forecasted a pre-tax operating margin of 20% over the next 10 years, as the company scales and benefits from an increasing amount of cross-selling between its products.

Tesla stock valuation (created by author Ben at Motivation 2 Invest)

Given these factors I get a fair value of $216 per share, the stock is trading at ~$109 per share at the time of writing and thus is ~50% undervalued.

As an extra data point, Tesla trades at a Price to Sales ratio = 4.52, which is 52% cheaper than its 5-year average.

Risks

Elon Musk Selling/Twitter

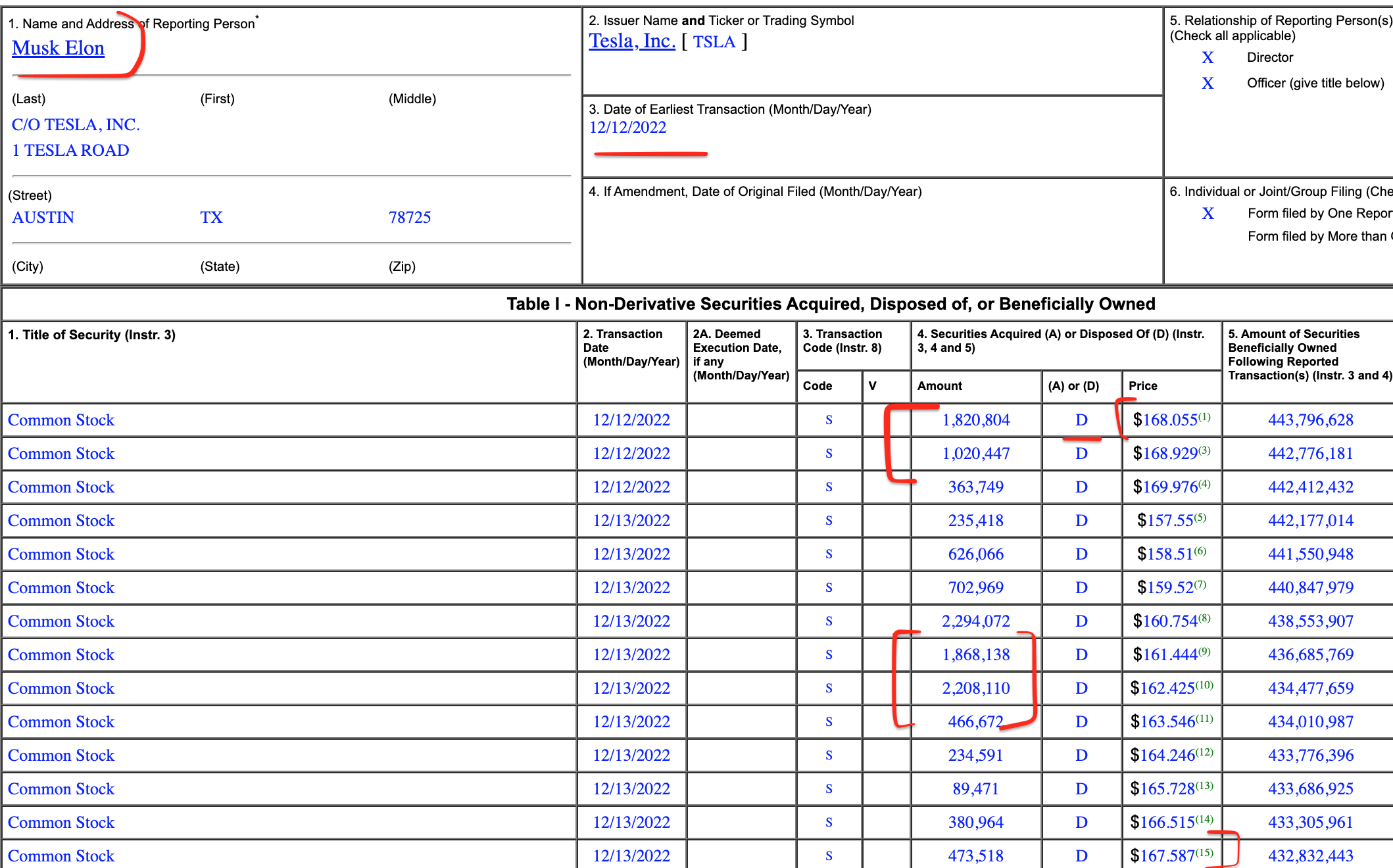

A key red flag is the continued sale of Tesla stock by Elon Musk. A mid-December SEC filing reports Elon Musk sold 22 million shares of Tesla stock, with a staggering value of $3.6 billion. Musk is known to have slept in Tesla’s factory and is very committed to the company, but when he repeatedly sells stock, it does contradict this narrative.

SEC filing (SEC/author annotation)

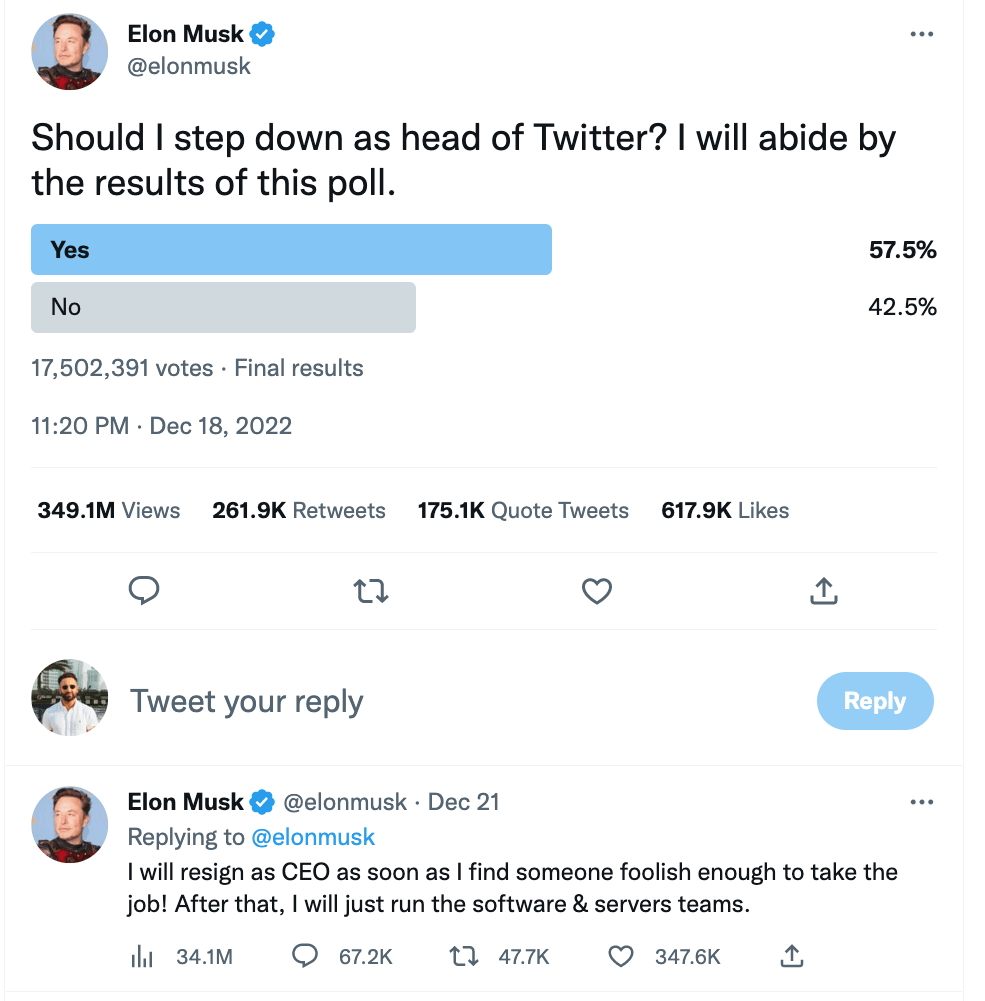

Musk may be selling shares to help pay down some of Twitter’s debt, which he has previously made comments about. Many investors (including myself) believe Twitter is a major distraction to Elon Musk’s mission at Tesla. In a recent vote on Twitter, 57% of people asked Elon to step down as the CEO of Twitter, which he said he will abide by when he gets a replacement.

CEO vote (Elon Musk Twitter)

Other risks include the forecasted recession and competition which I have previously discussed.

Final Thoughts

Tesla is a tremendous technology company with many competitive advantages from its manufacturing to technology and even its strong brand/community. Tesla has grown into its previously “high” valuation by continuing to generate strong financial results. Its stock is now deeply undervalued and thus this could be a great long-term investment. I do predict some short-term volatility over the next 12 months due to the recessionary environment, but Tesla’s technology advantages should keep them ahead.

[ad_2]

Source link