[ad_1]

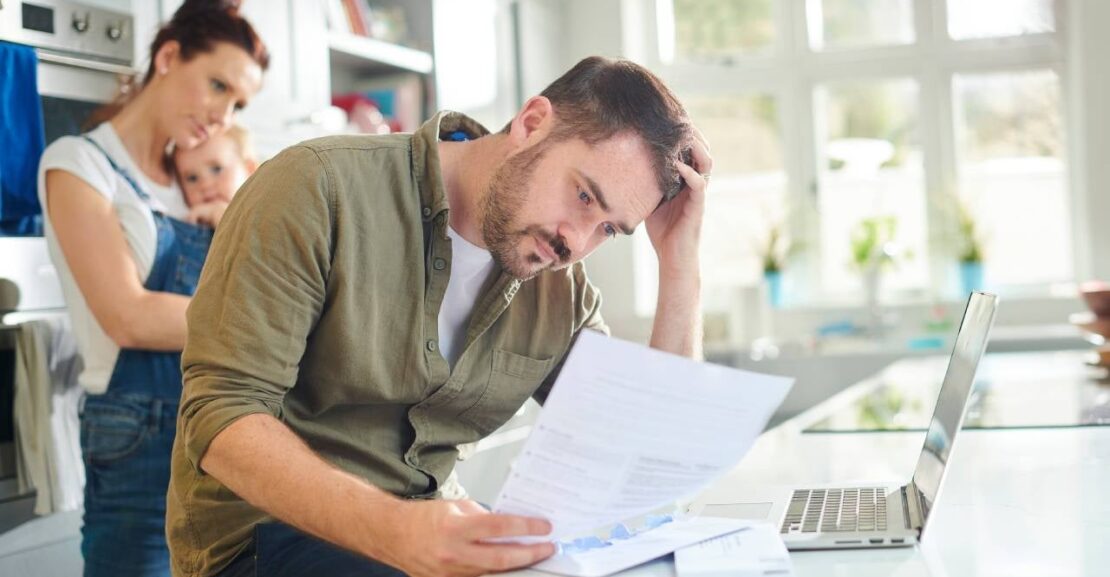

High inflation and a rising rate environment is sending the U.S. economy down an uncertain path. Economists now predict that there’s a 64% chance that the country will enter a recession in 2023. Interest rates and unemployment are also expected to rise, further straining the finances of millions of Americans who are already feeling the pinch.

Bankrate’s 2023 annual emergency savings report revealed that if faced with an unexpected loss of income, more than two in three Americans (68 percent) would be worried about their ability to cover a month’s worth of living expenses. Gen Zers show the most concern out of any age group with 85 percent worrying about having enough saved to live for a month, followed by 79 percent of millennials. Boomers are the least concerned with just 53 percent of them worrying about this scenario and Gen Xers are in the middle with 69 percent.

Saving in tough economic times can be challenging, but doing so is the best way to reduce borrowing or protect yourself in case of the unexpected.

Debt default statistics

- According to economists, there’s a 64% chance that the U.S. economy will enter a recession in 2023.

- Interest rates are also expected to rise above 5%, making borrowing more expensive.

- Personal loans currently have an average interest rate of 10.6%, which is slightly higher than pre-pandemic levels.

- Default rates for all credit products have increased by 0.23% since January of 2022.

- Rising inflation and a rising rate environment will increase serious delinquencies to levels not seen since 2010, particularly among credit card and personal loan products.

- Inflation, rising interest rates and employment changes have affected Americans’ ability to save, with 74% saying they’re saving less now due to one of these factors than a year ago.

- 85% of Gen Zers and 79% of millennials would be worried about their ability to cover a month’s worth of expenses if they were to lose their primary source of income.

- 1 in 4 Americans say they would rather use their credit card instead of tapping into their savings to cover a large emergency expense as they can pay it off over time.

- If hit with an unexpected $1,000 expense, only 43% of Americans would be able to cover it using their savings.

- 57% of Americans say the current economic conditions have negatively impacted their lives, with 53% delaying important financial milestones due to the state of the economy.

Best ways to borrow money

Most financial experts advise against borrowing when you’re in a tight financial spot, as this could lead to a vicious debt cycle. That said, if borrowing is your only viable option, make sure to weigh all the options available — paying special attention to interest rates, terms and fees, as there are better ways to borrow than others.

Safer lending options

When it comes to borrowing money in a time of crisis, these are some of the safest bets.

Friend or family member

If you only need to borrow a couple hundred dollars, asking one of your closest friends or a family member to lend you the money can be a great option. Although you may feel self-conscious or even embarrassed about asking for such a favor, borrowing money from someone you know will give you the flexibility to pay them back at your pace, without having to worry about dents in your credit report.

0% APR credit card

Some credit card companies offer consumers a 0 percent introductory offer in which any purchase they make over a specific period of time (usually between six to 15 months) is interest-free. However, any remaining amount that isn’t paid after the introductory period ends will accrue interest. Additionally, you’ll need excellent credit to qualify for these offers.

Personal loan from bank or credit union

When it comes to credit products, personal loans have one of the lowest interest rates available. Currently, the average interest rate for a personal loan is 10.6 percent compared to 20.15 percent, which is the average interest rate for credit cards. One of the benefits of using a personal loan to finance an emergency is that they have fixed interest rates and terms, so your payments will remain the same over the life of the loan. Besides that, many companies give borrowers between two and seven years to pay off their loans, making monthly payments more manageable.

On the downside, some lenders may charge origination fees or prepayment penalties, so make sure you take a look at the terms and conditions before you apply.

Buy now, pay later

Buy now, pay later or BNPL are a type of short-term installment loan that allows you to finance purchases, interest-free, for a specified period of time (usually between four and six installments). Although these loans are issued based on credit, you don’t need an excellent score to qualify. That said, if you fail to repay your entire loan after the interest-free period, you will be charged interest on any remaining amount. Additionally, these loans lack liquidity and can only be used at select stores.

Apps that let you borrow money

If you’re in need of some quick cash, a cash advance app could be the answer. These apps allow you to borrow money against your next paycheck and many of them don’t charge any additional interest or fees. However, you must be careful when using them, as they could lead to overspending.

Still, if this is an option you’d like to explore, here are some of the apps you could try:

Brigit

Designed as a budget management app, Brigit also allows members to access up to $250 instantly through its Instant Cash feature. The company doesn’t require you to pass a credit check to access this feature nor does it charge any late payment fees. However, users must pay a monthly subscription fee of $9.99 in order to access the Instant Cash feature.

Chime

To access a cash advance through Chime, you’ll need to have a checking account with the company. Once you have that, you’ll have access to the SpotMe feature, which allows you to overdraw your account by as much as $200, without any fees.

Dave

Dave is a digital banking platform. Among its services, the company offers a feature called ExtraCash, which allows users to get a cash advance of up to $500, without any interest or fees.

Payday loans and other risky lending options

There are certain types of emergency loans that should be avoided at all costs. That is because they’re highly risky products that offer unfair terms and extremely high interest rates that make it almost impossible for borrowers to repay their debts. These are two of them.

Payday loans

Payday loans allow borrowers to take out small amounts of cash (usually not more than $500) in exchange for extremely high interest rates and fees. Although some states limit interest rates to 36 percent, in others, like Texas, borrowers can expect to pay as much as 664 percent on interest. What’s more: only 14 percent of consumers who take out these loans are able to pay them back, which is why you should refrain from using them altogether.

Car title loans

When you take out a car title loan, you’re using your vehicle as collateral. These loans are usually short-term (no more than 30 days) and you can borrow up to 50 percent of your vehicle’s value. Car title loans come with exorbitant fees and interest rates as high as 300 percent and, if you don’t pay back your loan, you could lose your vehicle.

How to budget better

Budgeting during uncertain economic times can be more challenging than usual, as there are many variables that are out of our control.

Ralph Bender, CEO and founder of Enduring Wealth Advisors says that, when things are tight, the most effective way of budgeting is to prioritize what’s necessary (food, healthcare, shelter, etc.) and cut back on everything else.

“Unfortunately, many of the reasons we get into trouble is that we get locked into contracts for ‘desired’ things,” Bender adds.

Mac Gardner, founder and CEO at FinLit Tech, says that if you have debt, communication with your creditors is key. “If you see tough financial times ahead and you have a loan or financial obligation, be proactive and reach out to that institution. They will be more receptive to customers that reach out to explain their situation and look for ways to service the debt obligation.”

He also adds that It’s important during hard times to keep cash flow going, as many banks won’t lend to those without liquidity — even in case of an emergency.

“In today’s gig economy you can generate cash flow through ride sharing platforms like Uber or Uber eats. If you’re a collector, it may be wise to value your collection and utilize tools like eBay or other platforms to create liquidity,” Gardner says.

-

The two surveys referenced above were commissioned by Bankrate.com. Here’s how we got the results:

- Bankrate’s 2023 annual emergency savings report. This study was conducted for Bankrate by SSRS on its Opinion Panel Omnibus platform. The SSRS Opinion Panel Omnibus is a national, twice-per-month, probability-based survey. Interviews were conducted from December 16-19, 2022 among a sample of 1,028 respondents in English (1,003) and Spanish (25). The survey was conducted via web (998) and telephone (30). The margin of error for total respondents is +/-3.5 percentage points at the 95% confidence level. All SSRS Omnibus data are weighted to represent the target population.

- Survey: Majority of Americans delaying financial milestones, opting out of activities or events because of the state of the economy. Bankrate.com commissioned YouGov Plc to conduct the survey. All figures, unless otherwise stated, are from YouGov Plc. The total sample size was 2,442 adults. Fieldwork was undertaken between October 19-21, 2022. The survey was carried out online and meets rigorous quality standards. It employed a nonprobability-based sample using quotas upfront during collection and then a weighting scheme on the back end designed and proven to provide nationally representative results.

[ad_2]

Source link